Matthew Scullion is crystal clear that the turning point for the UK software company he founded was when it won the backing of two US venture capital firms.

In 2018, Scale Venture Partners and Sapphire Venture led a funding round in Matillion, then a seven-year-old start-up headquartered in Manchester.

UK investors contributed a small amount, but Scullion credits the injection of Silicon Valley cash and knowhow for helping propel Matillion into a select club: one of the UK’s unicorns, or private companies worth at least $1bn.

“[The US venture capital firms] want me to build the biggest company I can and to die trying,” explained the 45-year-old entrepreneur.

Yet for those City executives, business leaders and investors pursuing a radical reboot of Britain’s capital markets to reverse a multiyear decline in listings and turn start-ups into global champions, Scullion’s experience exposes many of the challenges they face.

Rebooting Britain’s capital markets

This is the second in a two-part series examining efforts to revive London’s stock market and reform a risk-averse pension system.

They include convincing often wary domestic pension funds to back start-ups and developing more investment funds with the nous, record and ambition to help entrepreneurs build their businesses.

In an election campaign whose final days have been dominated by a betting scandal, the future of the pension industry and how to grow world-leading companies have had little oxygen, but are on the agenda of the Conservatives and Labour party.

Last year, chancellor Jeremy Hunt set out plans to lift pension returns and investment in UK businesses. The so-called Mansion House reforms included a plan to give pension funds more firepower through pooling smaller ones as well as overhauling local government schemes.

The Labour party, which polls put on course for a victory in the general election on July 4, has promised to review the pensions industry, although has yet to provide details.

However, calls to force pension funds to funnel more of their investment into UK companies, public or private, have drawn fierce criticism. Opponents say it would risk hurting pensioners’ retirement pots by narrowing the choice of investments available to funds.

“We will invest wherever is going to achieve the best outcome,” said Andy Briggs, chief executive of FTSE 100 Phoenix Group, the UK’s largest long-term savings and retirement business. Although in favour of encouraging investment in Britain, “we would not be in favour of any form of mandation towards the UK”, he added.

For Sir Jonathan Symonds, chair of FTSE 100 drugmaker GSK, lifting investment in high-growth private companies is a prize worth fighting for.

Over four decades in the pharmaceutical industry, Symonds has witnessed the obstacles young companies, many of which start life within the country’s universities, confront in trying to scale up.

“We have a wonderful life sciences industry and one of the largest pools of capital in the world with our pensions industry, but they’re parallel universes,” said Symonds, who feared that future generations of retirees would be denied the financial rewards of UK innovation.

“We’ve got to support UK innovation with UK capital,” he added. “What we want is the UK, in its broadest form — individuals, companies, regions, universities — benefiting from or participating in the success of UK science and innovation.”

Fred Cohen, co-founder of venture capital firm Monograph Capital, which backs biotechs on both sides of the Atlantic, has seen promising UK groups snapped up by overseas buyers.

In 2022, MiroBio, a therapeutics company backed by Monograph that was spun out of the University of Oxford, was sold to US drugmaker Gilead Sciences for about $405mn.

Monograph’s portfolio also includes gene therapy group AviadoBio, which began life at London’s King’s College, and Maxion Therapeutics, which is developing antibody drugs out of Cambridge university.

“The quality of science in the UK is on a par with Boston and San Francisco and yet the ability to translate that into biotech product and equity value creation has lagged meaningfully,” argued Cohen.

A government-commissioned report last year recommended tackling one possible cause of this through the adoption of standard market terms to speed up spinout negotiations and prevent universities holding on to too much equity in the businesses, which can make it harder to incentivise their management teams.

But Cohen said Britain also suffers from a dearth of “true risk capital and there’s not a lot of managers who are comfortable taking the risk that is required to manage that capital”. He added: “In the City of London there’s a lot of capital but it tends to be focused on low risk, low reward asset classes like gilts.”

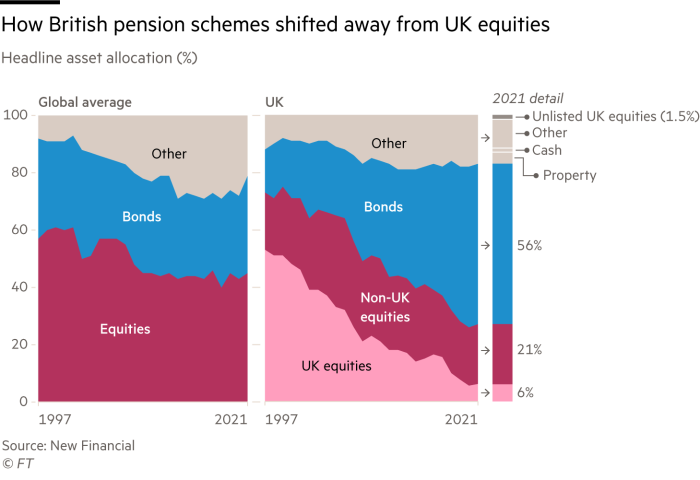

Low-risk government bonds have long been a staple of UK pension funds, but over the past two decades a combination of changes to accounting rules, tax and regulation has prompted managers to cut their allocation to equities.

An accounting standard introduced in 2000 required companies to calculate the surplus or deficit on their defined-benefit pension schemes annually and disclose any shortfall as a financial liability in their accounts.

In response, companies rushed to close defined-benefit schemes, which link a promised payout to an employee’s salary. As part of an attempt to avoid wild swings in potential shortfalls, pension schemes shifted funds out of equities and into less volatile bonds.

According to the Thinking Ahead Institute, UK pension funds had 26 per cent of their assets in equities at the end of 2023, down from 46 per cent a decade earlier. Within that, the share dedicated to UK stocks is much lower.

For those trying to lay the foundations of a revival in the UK’s capital markets, making London a more attractive destination for initial public offerings is an important yardstick of success.

According to Michael Tory, co-founder of advisory boutique Ondra Partners, a failure to do so would mean that for any investor looking to exit a UK private company, “the only viable routes will be either an IPO overseas or a trade sale to a foreign buyer”.

Proponents of a shake-up, however, say increasing pension funds’ risk appetite is critical to a wider renaissance, arguing it would both lift returns for retirees and help generate a source of domestic funding for start-ups.

Taavet Hinrikus, the co-founder of London-listed fintech Wise, is among those making the case.

“If UK pension funds are discouraged or restricted from investing in these asset classes, they are less competitive,” said Hinrikus, who after stepping down from Wise set up Plural, which backs European start-ups. “We need to find incentives to get pension funds to invest in non-public assets.”

Investors in US venture growth funds are predominantly domestic pension funds and endowments, he added.

Although there has been little focus on such questions in the election campaign, Briggs at Phoenix said governments would ultimately have to address how the pension industry can better serve retirees.

More than 80 per cent of Britons were not saving enough to maintain their living standards in retirement, according to a 2022 report from Phoenix. The issue has become more pressing as, over the past two decades or so, more companies have adopted defined-contribution models, which ultimately leave employees bearing the risk for the size of their retirement pots.

Briggs said any changes to the pension system should have a twin focus: lifting savings rates through ramping up auto enrolment, and funnelling more money into private assets, a sprawling category encompassing private equity, infrastructure and venture capital.

It is a view echoed by John Graham, the president and chief executive of the roughly C$630bn ($460bn) Canada Pension Plan Investment Board, one of the world’s biggest investors in private assets.

“Private equity has been the biggest driver of returns for our portfolio,” said Graham. “I don’t think there’s extra risk — what you do give up is liquidity. Private markets work well when you have pooled assets with a long-term time horizon.”

Australian and Canadian pension funds have a much higher allocation to equities and private assets than those in Britain, which has boosted their returns. Over the past decade, the overall size of the UK pensions industry has grown at 2.9 per cent a year versus 4.2 per cent for Canada and 6.8 per cent for Australia, according to the Thinking Ahead Institute.

Like the call to make pension funds shift more money into UK assets, any move to increase their allocation to private assets would also be contentious, especially as higher interest rates raise questions about the sustainability of their returns.

The Bank of England has warned about a build-up of significant risks in some types of private assets, such as private equity. Regulators have also noted worries that private assets are being held on investors’ balance sheets at inflated values.

At the same time, investing in private assets is more expensive than allocating to bonds or equities strategies that track an index.

Steven Batchelor, a partner at Hg Capital, a UK buyout firm specialising in the software industry, argued that pension funds need the flexibility to invest in areas that deliver better returns after fees.

Without that, he said, “there is a danger that pension schemes operate on a penny-smart, pound-foolish basis — which ultimately hurts UK pensioners the most”.

Channelling more money into private assets, including start-ups, is a central tenet of the Mansion House reforms. They include an agreement by 11 of the UK’s biggest DC pension providers to target allocating 5 per cent of their default funds, or up to £50bn, to unlisted assets by 2030.

Yet in a sign of how heated the debate over the future of the pension industry has become, the providers stopped short of pledging to lift their investment in UK companies, whether public or private.

As the City awaits what polls suggest will be a first Labour government since 2010, some executives argue that the agenda remains too timid.

“We need to be much bolder,” said Peter Harrison, the chief executive of FTSE 100 asset manager Schroders, arguing for the need for ramping up auto enrolment in pension plans, tax credits to encourage investment and the full pooling of local government schemes. “That would change the playing field massively in favour of UK investment.”

Like Scullion, Harrison is a member of the Capital Markets Industry Taskforce, a group of 10 business leaders set up in 2022 to make the case for a sweeping overhaul of capital markets. For the entrepreneur from Altrincham, near Manchester, the chief aim is clear.

“You can have as good a public market set-up as you like,” said Scullion. “But if you don’t have companies to take public in the first place, then all of that’s for zip. The single most important thing we need to do is to learn how to build consequential companies as a matter of course.”